Structured Settlements

What is a Structured Settlement?

A structured settlement is a Canada Revenue Agency endorsed option to provide secure tax-free income to victims of wrongful injuries or wrongful death.

- Auto Accidents

- Medical Malpractice

- Sports Injuries

- Workplace Injuries

- Shooting Accidents

- Sexual Abuse

- Residential School Abuse

- Crime Compensation Awards

In a Structured Settlement in Canada the defendant or Casualty Insurance Company purchases an annuity from a major Canadian Life Insurance Company and the payments from that annuity are irrevocably directed to the injured party or claimant.

It should be noted that the annuity and the irrevocable direction can never be changed or collapsed once the settlement is finalised. The monthly payments are designed to sustain the injured party for a protracted period and the recipient is effectively protected from losing, wasting or even giving away the settlement funds. In most cases we recommend a lifetime plan. These Structured Settlements guarantee that the claimant will never run out or "outlive" the money.

The Life Insurance Company and The Defendant Insurance Company both guarantee these payments that are a combination of return of capital and the interest that is generated over the term of the annuity. The claimant receives all of these payments completely tax-free.

The three most important attributes of a structure are: The unchangeable nature of the payments, the guarantees from major Life Insurance Companies and the tax-free status of the payments.

"...within 2 months of settlement (awards, lotteries, sweepstakes, insurance, inheritance) 25% of the recipients had nothing left... and within 5 years of settlement 90% had nothing left."

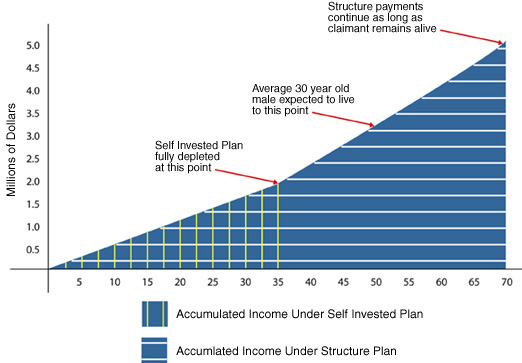

CUMULATIVE INCOME GRAPH

EXAMPLE

The following graph shows the reason to choose a structured settlement.

In this example we have selected a 30-year-old male claimant and compared the long-term outcomes of a cash settlement with a self-invested plan versus the structured settlement option.

Under both plans the injured party on an annual basis will receive identical after-tax cash but the structure has the advantage of lasting a lifetime.

Under the self-invested plan, tax eats into the principal and eventually there are no funds left.

STRUCTURED SETTLEMENT PLAN

Defendant Casualty Company purchases a structure annuity for $1,000,000.The annuity will create:

- Monthly Tax-Free Payments for Life.

- $41,000 total in year one and thereafter increasing at 2% per year.

CASH SETTLEMENT / SELF INVESTED PLAN

- Cash Settlement $1,000,000

- Amount Invested $1,000,000 Annual Return 5.5%

- Annual Management Costs 0.5%

- Other Taxable Income: nil

- Taxed at the current progressive rates

- Annual Withdrawal required $55,000 increasing at 2% per year to generate

- Annual After Tax Income of $41,000 increasing at 2.0 % per year.

LIFE EXPECTANCY ANALYSIS

StatsCan has determined from historical records that a 30-year-old male can expect to live another 46.8 years. This projection however does not take into account the fact that longevity is increasing significantly as a result of improvements in medicine and nutrition. Calculations based on historical rates of change in life expectancies indicate that, in this example, the life expectancy is probably closer to 50 years.

CONCLUSION

By the claimants 65th birthday, under the two plans, the after-tax cash income will be identical and the claimant will have received approximately $2,000,000.

Under the self-invested plan however the capital will be fully depleted at this point and all funding will stop as shown in the above chart.

Under the structured settlement plan the claimant will continue to receive the monthly payments, which continue to increase at 2%. If the claimant lives to the expected age the claimant will receive an additional $1,500,000 tax-free.